My friend Susan Kirkland is back again this month with some sage advice for those freelancing or running their own business in the creative world — trying to survive in an edgy economy.

![]()

My friend, the hoity-toity designer, bought several houses the last time the economic wheel hit dirt. He rented them out and had quite a nice piece of pocket change. When property values plummeted, unemployment rose and tenants decamped, he couldn’t pay the mortgage on some of those empty houses. He walked away. I was at his house one day when the phone rang. “Hello?” he answered, “yeah, just a minute, I’ll get him.” Then he set the phone down and continued our conversation on the dying art of marker comps. After about ten minutes, I reminded him about the caller on hold. “No worries, it’s just a collection agent. I like to tie up their line and let them sweat it out. After a few times, they just give up.” No fear here.

The Consumer Credit Protection Act* lays out the rules for collection agents. One thing you can do to end those calls is send a certified letter telling them to stop calling you. They are obligated by law to stop and if they don’t, you can sue them for 3 times the amount of money you owe them plus any punitive damages the court will allow.

Suits in ivory towers who purport to know all the answers about the world used to mystify me. You don’t have to be in a think tank or institution of higher learning to know that when the price of fuel goes up, everything that uses fuel in it’s production, transportation or storage will go up. Add Wall Street’s pressure on corporations to minimize operation costs (a.k.a. the cost of doing business) and the price of everything will double overnight. All those monthly reports of negative inflation were jolly juice to keep the masses happy. How robust is our economy when growth is one tenth of one percent (that’s one tenth of one one-hundredth for the math impaired)?

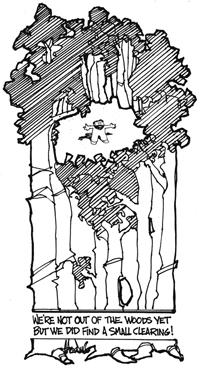

Almost everyone who is self-employed will face a time when they can’t pay the bills. (Don’t pat yourself on the back if you haven’t taken any risks) The hard part is to avoid wasting time debasing yourself over what you should have done or could’ve done to avoid the trauma of empty bank account syndrome. Hard times show what you’re made of; so use your creative advantage when dealing with the shortfall. One of the first freelance assignments I had was an illustration for a designer who was pressed to pay. See that guy standing in the clearing in the woods? He included it with his regular, small payments to remind them he was making an effort.

Almost everyone who is self-employed will face a time when they can’t pay the bills. (Don’t pat yourself on the back if you haven’t taken any risks) The hard part is to avoid wasting time debasing yourself over what you should have done or could’ve done to avoid the trauma of empty bank account syndrome. Hard times show what you’re made of; so use your creative advantage when dealing with the shortfall. One of the first freelance assignments I had was an illustration for a designer who was pressed to pay. See that guy standing in the clearing in the woods? He included it with his regular, small payments to remind them he was making an effort.

People in the collection industry are not above tricking you either. I know a guy who bought a new car, returned it to the dealer two years later because he couldn’t sell it to keep from losing it. The car company had given away so many incentives, he owed more than the car was worth. Seven years later, the car company is still plaguing him with collection efforts even though the statute of limitations has long expired. Why? Well, if they can get him to feel responsible and agree he owes the money, the statute restarts as if he bought the car yesterday. Don’t fall for it. No one can legally collect a debt after the statute of limitations runs out; that varies from state to state, so Google it.(*) And guess what—anything older than 6 months on your credit record (except for bankruptcy) must be removed at your written request because it’s no longer accurate.

Remember the throng of ads for cashing in on the equity in your house? That was right before the Credit card lobby got Congress to rewrite the bankruptcy law in their favor. Credit cards are unsecured, making them pretty much uncollectable; but if they can convince you to shift that debt into the equity of your house, hey, why not! They prefer you to be homeless to their taking a loss on a profit bigger than the national deficit. Oh, yes, I know, you owe the money and it’s your duty to pay it back—do the right thing. Are those interest rates right (fair and equitable compounded daily)? Until the common man has the same power the lobbyists wield when legislation is written, right and wrong won’t apply. If you are making the minimum monthly payment on all those credit cards, you are already in deep doo-doo.

One final note; don’t lose hope. Everybody has ups and downs, but not everybody shows it. That competitor who drives the Jag that you find so intimidating might still live at home. Make those cold calls, stay in touch with your industry connections, and business will reappear. The worst thing you can do is dig a hole and crawl into it—though that may be your gut reaction. Call your suppliers and see if you can work out an arrangement. Sometimes, they need design work or have clients who do. Big printers are usually willing to work out a trade when a regular customer gets in over his head. If worse comes to worse, remember that many successful people including Mark Twain, Walt Disney, Francis Ford Coppola, Frank Lloyd Wright and even the “you’re fired” guy all filed bankruptcy; so what. I know it’s hard when you’re a designer, art directing the perfection of your life; but remember that you’re not here to get by unscathed. You’re here to learn, grow, get beat up a little and see what kind of fabulous lines you can sculpt into that face to show where you’ve been and what you’ve learned.

Rock on.

Rock on.

Regards,

Susan Kirkland,

This article was originally published in 2007

Got questions about freelancing?

Got questions about freelancing?

Tired of working for someone else and doing the boss’ castoffs? Better get some good advice on how to protect yourself from those who would pillage and plunder your creative talents. Susan Kirkland wrote the book she needed when she first started out in advertising design to keep you from making some of the same mistakes.

Start and Run a Creative Services Business is filled with a full spectrum of Susan’s experiences over 25 years. Not an artist? You’ll be in stitches as you follow the pitfalls and adventures of self-employment. And if you’ve been freelancing for a while, you’ll find new information and a trustworthy mentor to stand by your side through thick and thin in Start and Run a Creative Services Business! Excerpts are available online at www.sdkirkland.com.

And, thanks to Susan for sharing this article, and thanks to YOU for reading it!

Don’t forget … we encourage you to share your discoveries with other readers. Just send and email, contribute your own article, join the Design Cafe forums, or follow DTG on Facebook!